Seatrade-Maritime: Fuel and peak season surcharges lift Transpac box rates

Published by Seatrade-Maritime

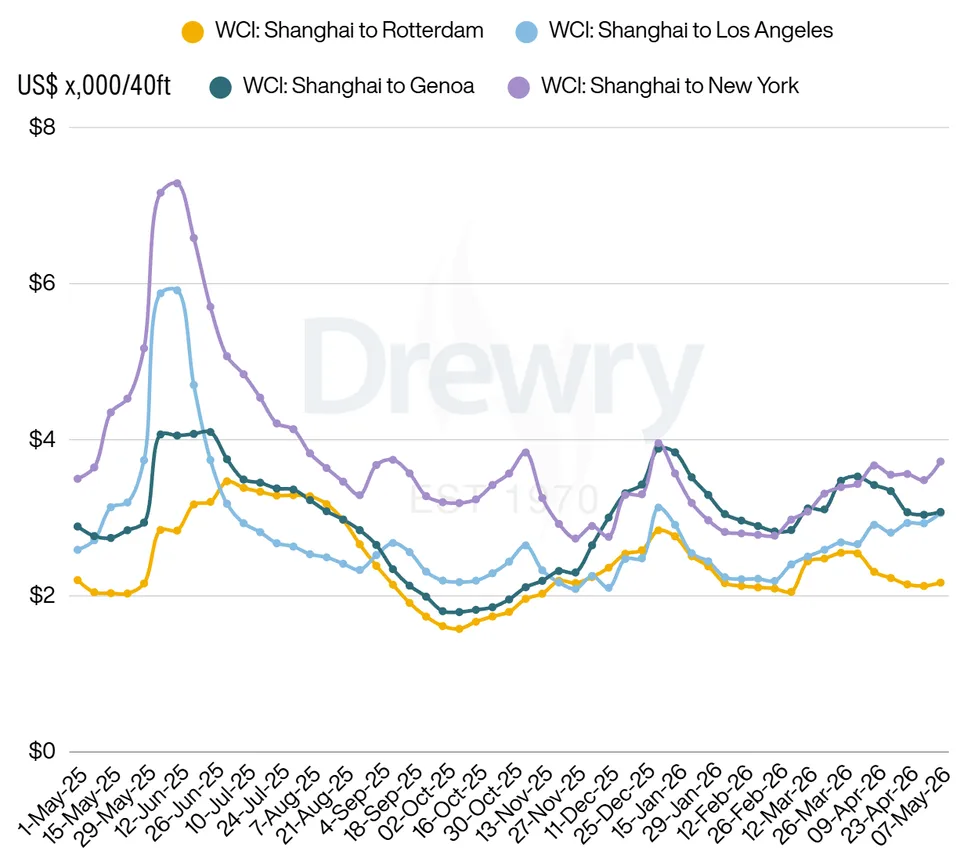

Drewry’s World Container Index (WCI) broke a three-week streak of declines on 7 May, recording a 3% increase in 40-foot container rates to $2,286.

The uplift was driven by Emergency Fuel Surcharges and Peak Season Surcharges bringing increased rates on transpacific routes — which Drewry expect will rise again next week — with milder positive movement on Asia-Europe trades.

The analyst reported a 7% rise in rates for Shanghai to New York to $3,721 per 40 ft container and a 5% increase for Shanghai to Los Angeles to $3,062. Examples of surcharge support included MSC adding $214 to its Emergency Fuel Surcharge on the Asia-US East Coast route to $644 per 40 ft container, and $195 on Asia-US West Coast to $467. CMA CGM introduced a Peak Season Surcharge of $2,000 from May 1.

Chart: Drewry World Container Index

Descartes’ analysis of April 2026 US containerised imports showed a 3.2% decline from March 2026 to 2.28m teu, a 5.5% drop compared to April 2025. Imports year-to-date were down by 5.0% on 2025.

China-origin imports of 680,778 teu were down 4.3% on-month and 33% lower than their peak in July 2024, the analyst said. Gains in imports from nations such as Thailand and Japan were unable to offset China-origin losses, leading to a 3.1% drop in US imports from its top 10 countries of origin.

“Trade relations with key partners, including the EU, India, and China, remain unresolved, reinforcing a global shipping environment defined by volatility, shifting sourcing strategies, and heightened cost uncertainty.”

Asia-Europe FAK rates challenge

Rates on Asia-Europe were more stable, rising by 2% on Shanghai to Rotterdam $2,170 per 40 ft container and 1% for Shanghai to Genoa to $3,075, according to Drewry. It forecast stable rates in the coming week and cast doubt on proposed FAK rates from CMA CGM, Hapag-Lloyd , and MSC of between $3,500-$4,500 per 40 ft container for Asia–North Europe, and between $4,500-$4,600 Asia–Mediterranean. Due to come into effect from 15 May, Drewry said “successful implementation remains unlikely due to weak demand and excess capacity, which continue to create a supply–demand imbalance.”

Middle East impacts

In its Intra-Asia Index update, Drewry said softening rates for Shanghai-Jebel Ali may indicate a market finding equilibrium within Middle East disruption, while rising rates on Shanghai to North, South, and Southeast Asia indicate tighter supply on those routes. Overall, the index of 18 trade routes rose for a fourth consecutive week to $925 per 40 ft container.

Drewry said carriers remained cautious on routing and operations amidst the situation in the Middle East and Strait of Hormuz.

Commenting on its impacts in the US, Descartes said US imports from the Gulf are primarily energy, fertiliser, and aluminium. “While these goods represent a smaller share of total containerised imports, they are disproportionately important to downstream supply chains. Disruptions to these flows can create ripple effects across multiple industries, including manufacturing, automotive, construction, and consumer goods,” said Descartes.

Related Posts